This is how to get rid of closed accounts on credit report.

When it comes to your credit report, you want the best score possible. Part of your credit report revolves around closed accounts and you’ll need to understand the impact of closed accounts on their credit scores. When an account is closed, it can stay on your credit report for up to 10 years. A closed account may also reduce the average age of accounts, lowering your credit score.

Fortunately, you can get rid of these outdated closed accounts from your reports if you want them gone once and all. This article will discuss how closed accounts affect your credit and show you how to remove those old negative items from your reports so that you can start fresh with new positive scores!

How Closed Credit Accounts Affect Your Credit

Your credit score is based on various data, including your payment history, credit inquiries, credit utilization, credit age, and the multiple types of credit accounts.

How much weight each factor receives in determining your FICO score depends on how important that factor is to a particular lender. For example, a car loan may be more concerned with your payment history than with how many retail stores cards you have open. The credit bureaus then use this data to calculate where your score falls.

Here is what happens when you close your credit account:

Negative items, such as late payments or collection accounts, stay on your credit reports for years and can be extremely detrimental to your credit scores and long-term financial health. For instance, late payments stay on your credit for seven years before they can be removed.

TransUnion and Equifax credit reports include closed accounts with no negative information for ten years from the reported closed date. Generally, this means that good credit data stays on your report longer than most negative stuff, such as late payments.

What Can You Do to Improve Your Credit Score?

If you are looking for ways to improve your credit scores, you have innumerable options. First, pay off outstanding balances on any credit card accounts that are close to being maxed out or are already at maximum capacity. Also, ensure you maintain a low credit card debt.

Experts advise against having credit card balances that exceed 30% of your available credit, but keeping them at or below 10% is ideal for credit scores. If possible, try to pay off your entire credit card bill every month.

Next, be sure that all of your payments are made on time every month. If you want to increase your credit score even more, try not to open new lines of credit too frequently.

When Should You Delete a Closed Account From Your Credit Report?

Most people wonder if they can erase closed accounts from their credit history and when they should do so.

Well, the only time you should make an effort to have a closed account removed from your credit report is if there is any misleading information published about it. In particular, if the negative information is inaccurate.

There are a few ways to delete or at the very least try to erase incorrect information from your credit reports. Here are the steps to delete closed accounts from your credit report.

1. Make a formal complaint about the errors.

You can combat bogus information on your credit reports with the Consumer Financial Protection Bureau (CFPB), as well as the credit bureaus and the business that provided the incorrect data.

Suppose information from a closed account shows up on your Experian credit report; you should dispute it with Experian and the lender that reported the false data, such as a credit card company.

Disputing incorrect information online may be as easy as providing your name, address, and phone number, along with the specifics of your complaint. You should include the following details in addition to the contact information:

- Account numbers for disputed accounts

- A written statement of why the inaccurate information is incorrect.

- A printout of your credit report with errors underlined

- Any documentation that demonstrates the legitimacy of your claim, such as payment receipts

Once you gather this information, you will send it to the credit reporting company via mail.

After receiving your written dispute, the credit bureau has 30 days to finalize its investigation. The agency may contact you during this period if it needs more information. If you can confirm the accuracy of the disputed information, it will be removed from your report. Otherwise, they will contact you with their position on your dispute.

2. Wait for your accounts to drop off.

If you’re not going to dispute errors, your closed accounts will drop off your credit reports after a while. But how long will they remain on your credit history?

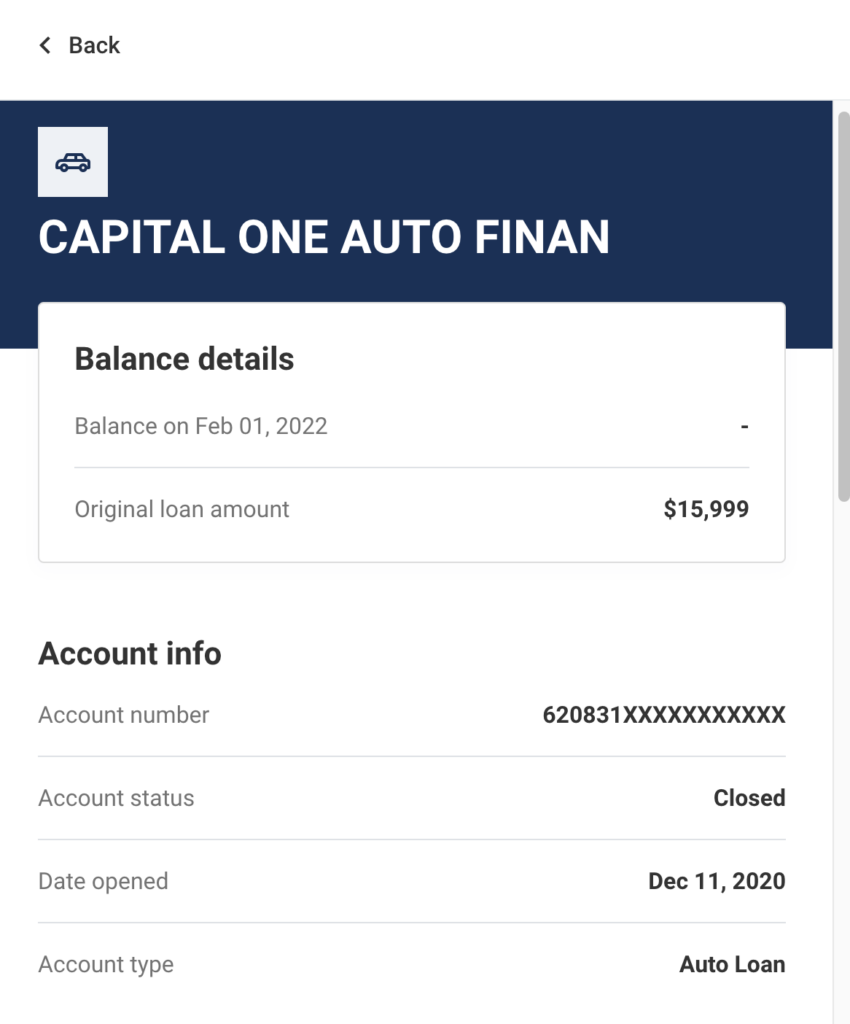

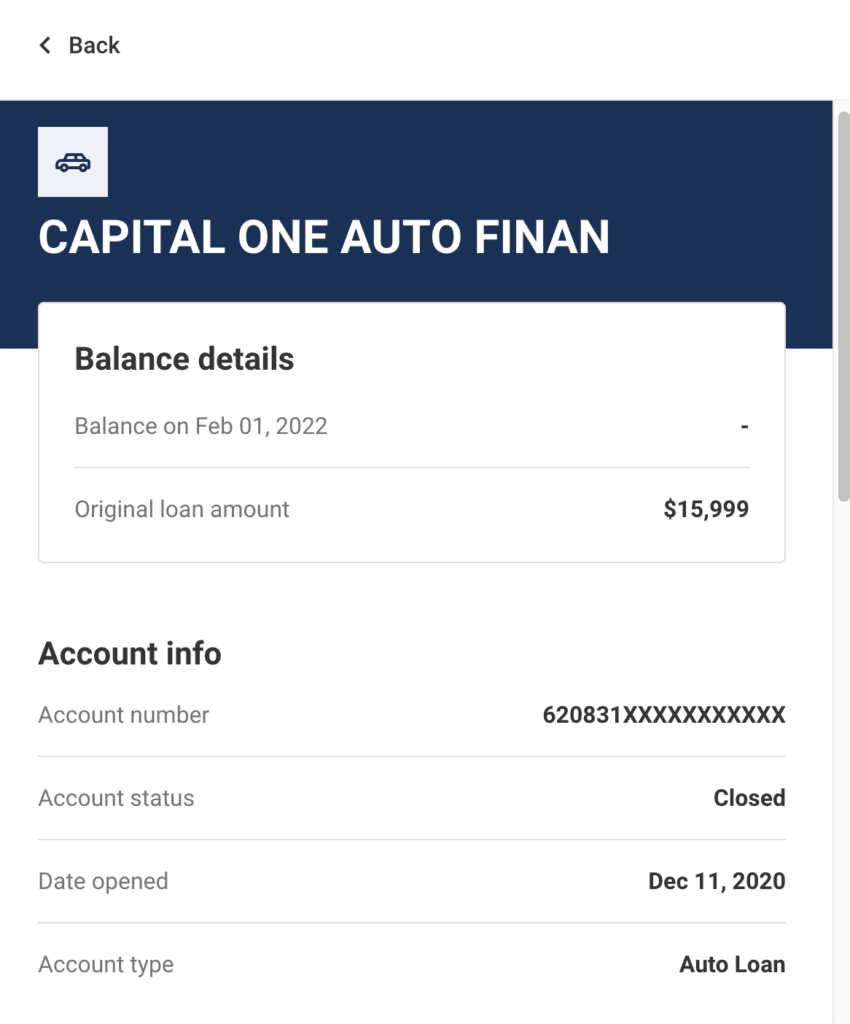

Closed accounts in good standing can stay on your report for ten years from the date it was reported as being closed. In contrast, negative information, such as late payments and collection accounts, can remain on your Experian credit report for seven years.

AnnualCreditReport.com gives a free copy of your credit reports from all three credit agencies once every 12 months. This can be of help if you want to check which accounts are still on your credit.

3. Pay for Delete.

If the negative information on your credit reports is accurate, but you want to improve your score as quickly as possible, pay for delete may be a good option.

Paying for deletion means paying off a delinquent account with a lender or collection agency. In turn, the creditor agrees to “delete” this paid account from your credit report. The creditor will then close the account and report it as “settled” by the consumer. Because the account is paid and no longer delinquent, it should reflect positively on your credit.

Although settled accounts should not have any other negative impact on your credit history, you may still want to monitor the performance closely. This is because some creditors will re-list settled accounts as new ones seven years after they are closed – which will show up on your credit report as an open account.

4. Goodwill Letter

If you have no luck with the credit bureaus or creditors in getting negative information removed from your credit report, you can still try a goodwill letter to the creditor. Goodwill letters are written requests asking the creditor for “goodwill consideration,” which essentially means they are willing to forgive a debt in exchange for payment.

When writing a goodwill letter, it’s important to keep in mind that specific situations might make it more successful – Such as a serious sickness or injury that prevented you from working for a lengthy time frame, and you defaulted on a credit card or a loan.

Creditors may also consider external factors such as your previous payment performance and whether you’ve made any genuine efforts to pay since you defaulted.

How successful you are at getting these items removed from your credit reports largely depends on how much you’re able to pay and whether the creditor views your account as valuable.

Conclusion

Negative information on your closed accounts affects your score. While it eventually drops off your report after several years, you can still have it removed earlier. If you’re experiencing financial difficulties or have been in a long-term debt management plan with creditors, you can consider the aforementioned methods of getting rid of closed accounts on your credit report. After that, you should also make all your payments on time. This will ensure that you maintain a good payment history and keep it in good standing, increasing your credit score over time.