When you find yourself in a situation where you’ve been served with legal papers for an unpaid debt, it can be an intimidating and stressful experience.

Debt-related legal actions can have serious consequences, including potential wage garnishment, damage to your credit score, and even legal fees.

Let’s discuss the various aspects of what happens when you get served papers for debt, from understanding the legal process to exploring your options for resolution.

Understanding Debt Collection and Lawsuits

Debt Collectors and Debt Collection Agencies

Debt collectors play a crucial role in the debt collection process. They are individuals or agencies hired by creditors to recover outstanding debts. These collectors are often persistent in their efforts to secure payment.

Original Creditor vs. Debt Collection Agency

The original creditor is the entity you initially owed the debt to, such as a credit card company or a medical provider. When you fall behind on payments, the creditor may sell your debt to a debt collection agency. Understanding who is pursuing the debt can be essential in determining your next steps.

Debt Lawsuits and Legal Action

When all other collection efforts fail, creditors or debt collection agencies may resort to legal action. This usually involves filing a lawsuit against you in civil court, seeking to obtain a court order for the repayment of the debt.

The Legal Process of Debt Lawsuits

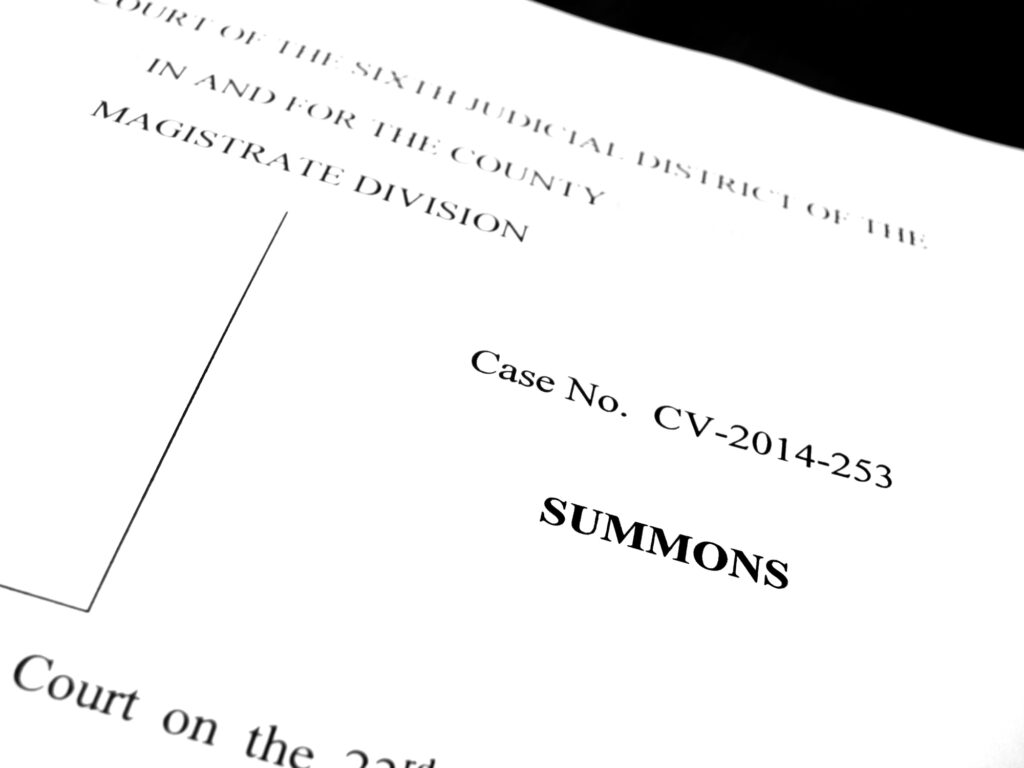

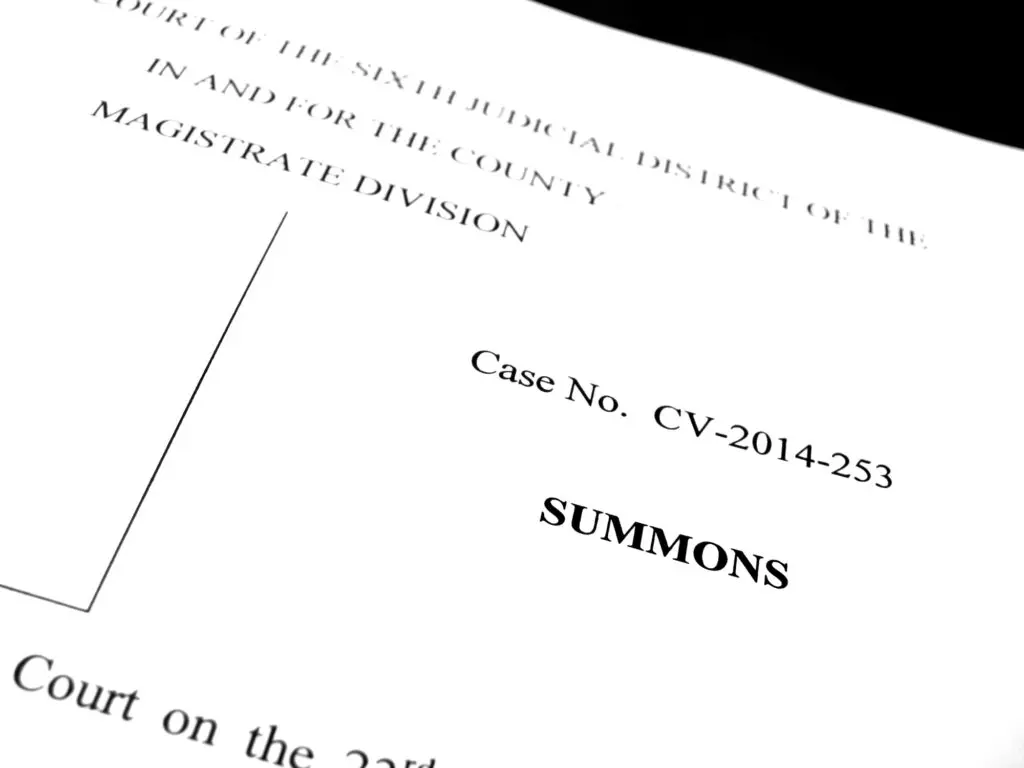

Service of Legal Documents

The first indication that you’re facing a debt-related lawsuit is being served with legal documents, typically referred to as a “court summons” or “complaint.” These documents outline the creditor’s claims and initiate the legal process.

Responding to a Court Summons

Ignoring a court summons is not advisable. You must respond within a specified time frame, usually 20-30 days, depending on your state’s laws. Failing to respond can result in a “default judgment” against you, which means the court automatically rules in favor of the creditor.

Affirmative Defenses

In your written response to the complaint, you may assert “affirmative defenses.” These are legal arguments that challenge the creditor’s claims, such as disputing the debt’s validity or asserting that the statute of limitations has expired.

Court Costs and Legal Fees

As the defendant in a debt lawsuit, you may be responsible for court costs and, in some cases, the creditor’s legal fees if you lose the case. It’s crucial to understand your potential financial obligations.

Trial Date and Court Proceedings

If the case proceeds to trial, you’ll need to prepare for your court date. This can be an intimidating experience, but it’s essential to present your side of the story and defend your legal rights.

Debt Resolution Options

Negotiating with Creditors

Before the case reaches trial, you can explore the possibility of negotiating with your creditor or debt collection agency. This may involve setting up a payment plan, making a lump-sum payment, or even settling for a reduced amount.

Debt Management Plans

Working with a credit counselor or a debt management agency can help you create a structured plan to repay your debts. This can be a good option if you have multiple debts and need professional assistance.

Debt Settlement Lawyers

If negotiations fail and you’re facing a court case, consulting with a debt settlement lawyer can be beneficial. They can guide you through the legal process, advise you on the best course of action, and potentially negotiate on your behalf.

Bankruptcy Protection

In some cases, filing for bankruptcy may be the best option for individuals overwhelmed by debt. Bankruptcy can provide a fresh start, but it also has long-term consequences, so it should be considered carefully.

Protecting Your Legal Rights

Federal Fair Debt Collection Practices Act (FDCPA)

Under the FDCPA, consumers have rights that protect them from abusive or unfair debt collection practices. Knowing your rights can help you deal with debt collectors and collection efforts.

Statute of Limitations

Each state has a statute of limitations that determines how long a creditor can legally pursue a debt. If the debt is beyond this time period, it may be unenforceable in court.

Automatic Stay in Bankruptcy

Filing for bankruptcy triggers an “automatic stay” that temporarily halts debt collection efforts, including lawsuits and wage garnishment. This can provide relief and time to evaluate your financial situation.

State-Specific Considerations

State Laws and Regulations

Debt collection laws vary from state to state. It’s crucial to understand your specific state’s laws and regulations, as they can impact the debt collection process and your legal options.

New York as an Example

Using New York as an example, we’ll explore how state laws can influence the debt collection process. New York has specific laws and regulations that provide additional protections to consumers.

Steps to Take When Served with Debt Papers

Step 1: Review the Legal Documents

When served with debt papers, the first step is to carefully review the court summons and complaint. Ensure that the information is accurate, and consider seeking legal advice.

Step 2: Consult an Attorney

If you’re unsure about how to respond or negotiate with the creditor, consulting with an attorney experienced in debt collection cases is a wise move. Many attorneys offer free consultations to assess your situation.

Step 3: Gather Information

Collect all relevant information about the debt, including any correspondence with the creditor, payment history, and a copy of the complaint.

Step 4: Respond Promptly

Timely response is crucial in a debt lawsuit. Failure to respond can result in a default judgment, which can have severe consequences.

Step 5: Explore Debt Resolution Options

Consider negotiating with the creditor, exploring debt management plans, or consulting a debt settlement lawyer to determine the best course of action.

Step 6: Attend Court Proceedings

If the case proceeds to trial, attend all court hearings and present your case. Be prepared to provide evidence and assert your rights.

The Importance of Your Financial Situation

Your financial situation is at the center of the debt resolution process. Understanding your budget, income, and expenses is crucial to making informed decisions.

Protecting Your Credit Score and Report

A debt lawsuit can have a negative impact on your credit score and report. It’s essential to take steps to mitigate this damage, such as negotiating a settlement or creating a payment plan.

Conclusion: Navigating Debt Lawsuits with Confidence

Facing a debt lawsuit can be daunting, but understanding the legal process, your rights, and your options for resolution can help you navigate the situation with confidence. Whether you choose to negotiate with creditors, seek professional legal advice, or explore bankruptcy protection, the most important thing is to take action and address your debt in a way that aligns with your best interests and financial situation.

Remember that each case is unique, and seeking legal advice tailored to your circumstances is often the wisest course of action. By taking proactive steps and making informed decisions, you can work toward resolving your debt and achieving financial stability.

For more information and assistance, consider reaching out to debt resolution attorneys or organizations that offer free legal help. They can provide you with additional information and guidance specific to your situation.